FTA Insurance WINS multiple

5-Star Excellence Awards

The professional indemnity market has been a tough nut to crack for some time now, with policy excesses and premiums spiraling upwards, low capacity, tighter policy conditions and, in some sectors, a limited number of insurers who are willing to provide cover.

In its recent Professional Indemnity Market Update, Willis Towers Watson pointed to a widespread reduction in capacity as a significant hurdle in a market that has been hardening since 2017, noting that “reductions from $20m to $10m, or even as little as $5m in some cases, are common”. Premium hikes are also rampant in today’s market, according to WTW, which pointed out that rises of 50% and 100% are common and noted that “we have even seen increases as much as 2,000% in some extreme cases”.

Events in the London market have also had an impact. When Lloyd’s undertook its Decile 10 review in 2018, PI was identified as one of its worst-performing classes, which led to a big drop in capacity for the Australian market that continued into 2020. Insurers responded by being more selective about who they will cover; others opted out of renewing binders in certain professional indemnity markets.

Yet the need for insurance for those providing advice or a service, in the event of legal action claiming malpractice or misconduct, has never been more keenly felt. Not only is PI insurance a mandatory requirement for professions such as lawyers, doctors, real estate agents and stock agents, but it’s also becoming increasingly critical for a wide range of other occupations, from contractors to copywriters. The cost of being uninsured or underinsured can be crippling in the event of a claim – it can even put companies out of business.

The hardest markets

Two segments of the PI market have been particularly hard-hit. Driven in part by a surge in shareholder litigation, directors & officers (D&O) cover is suffering from a vola-tile and reactive market. A September 2020 report by the Institute of Directors, Marsh and MinterEllisonRuddWatts noted that a host of local and overseas insurers have with-drawn from the D&O market and estimated that capacity in the London market alone is 50% less for ASX-listed companies than it was in 2017.

The construction sector has also been battered by insurers limiting their cover, according to the WTW report, which noted that “the construction industry has borne the brunt of this tightening as insurers seek to limit cover for contractual liabilities that extend risk beyond the usual standard of care that is expected of professionals in the sector”.

There are notable exceptions – the Victorian Government announced in February that it had taken out $6.9m in professional indemnity insurance coverage for surveyors, project managers and other contractors engaged in the state’s $600m cladding rectification works on faulty high-rise buildings. The exclusion-free cover was a rare and welcome phenomenon at a time when many PI insurance policies contain exclusion clauses for defective cladding because of the potentially astronomical cost of claims.

“Brokers need to always consider what type of risks an underwriter is winning and whether the client they are trying to place is consistent with that and fits into that portfolio” – Christian Garling, FTA Insurance

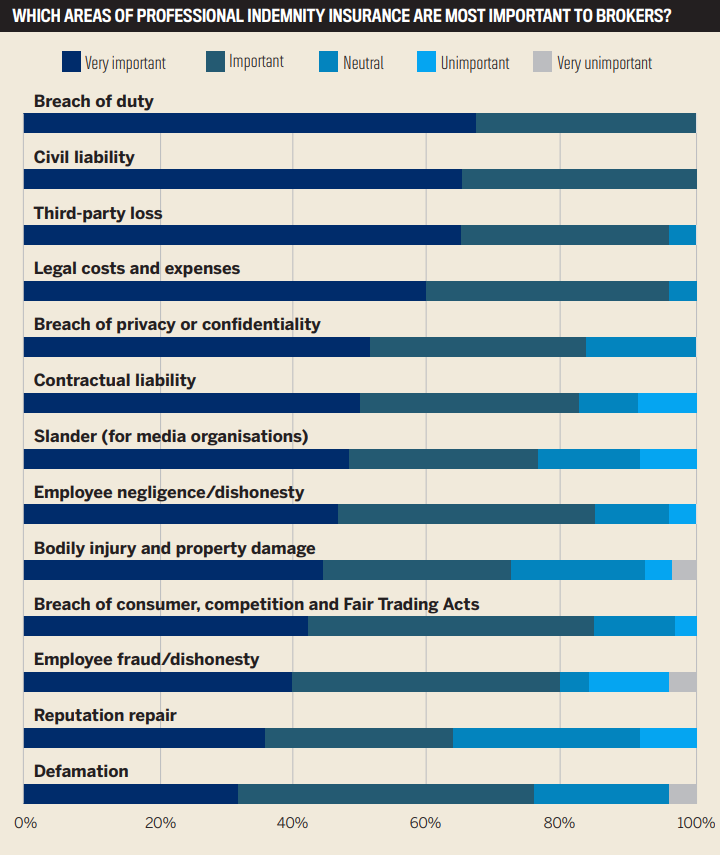

Picture source: Insurance Business Magazine “5-Star Awards 2021 : Professional Indemnity Insurers

A chance for brokers to shine

Despite the challenging conditions, there is no shortage of optimism among this year’s 5-Star Professional Indemnity winners.

CLICK HERE TO SEE WHICH CATEGORIES FTA INSURANCE WON

A hard market creates opportunities for brokers to show the value of their expertise and professionalism. It creates an opening for brokers to educate their clients on the conditions of the hardening market and to manage their expectations when they are unable to get terms or when they experience a significant increase in their premium. A broker can guide their clients through to process, try to achieve the best result possible and create new relationships or cement their existing ones.

Christian Garling, managing director of Sydney-based FTA Insurance, adds that with premiums increasing and terms tightening, many insureds are reviewing their coverage to make sure they have market-competitive terms.

“If a broker is staying in contact with potential clients, then this provides an opportunity for the broker to show what they can achieve,” Garling says.

Brokers can also play an invaluable role by pointing out potential gaps in a policy, he adds. “With many clients using online systems, they can receive inappropriate terms, and this is a great opportunity for a broker to show their expertise by pointing out the deficiencies in cover. Alternatively, [they can advise] on new products and exposures that the client might not have appreciated, [such as] cyber.”

Brokers can also play an invaluable role by pointing out potential gaps in a policy, he adds. “With many clients using online systems, they can receive inappropriate terms, and this is a great opportunity for a broker to show their expertise by pointing out the deficiencies in cover. Alternatively, [they can advise] on new products and exposures that the client might not have appreciated, [such as] cyber.”

One of the most important things for a broker is to fully understand the client’s business, exposures and requirements to obtain adequate coverage. It starts with a fully completed proposal form which is essential to insurers to assess the risk. It is important for brokers to ensure that their clients have answered all these questions correctly and that they provided accurate information such as their business activities to which the risk relates. This can make or break how the risk is assessed by underwriters. Sometimes a risk can simply be declined due to an incorrect completed proposal form.

If you really want your client to stand out, you can provide additional information on top of a completed proposal form. Additional information is often welcomed by insurers, such as copies of standard contracts or CV’s, to get the risk quicker over the line and make your client stand out. Once all of those boxes are ticked, the final step is to engage with the underwriter to get the best possible terms for your client. Keep an open dialogue with the underwriter and discuss the terms and premium wanted. A few phone calls back and forth between the broker and underwriter can often do wonders.

As for the likelihood of more insurers pulling out of the PI market, Garling believes the situation has stabilised for now – although he notes that there are still some very large players “taking corrective action” on their portfolios.

“Brokers need to always consider what type of risks an underwriter is winning and whether the client they are trying to place is consistent with that and fits into that port-folio,” Garling says. “If you see an under-writer applying little in the way of under-writing filter or targeting risks that are distressed, then you can expect that portfolio to experience significant rate movements or even a withdrawal of capacity. However, if you see an underwriter targeting low-hazard and low-exposure business, this will give a broker and their client confidence that the rates should stay consistent and capacity be available into the future.”

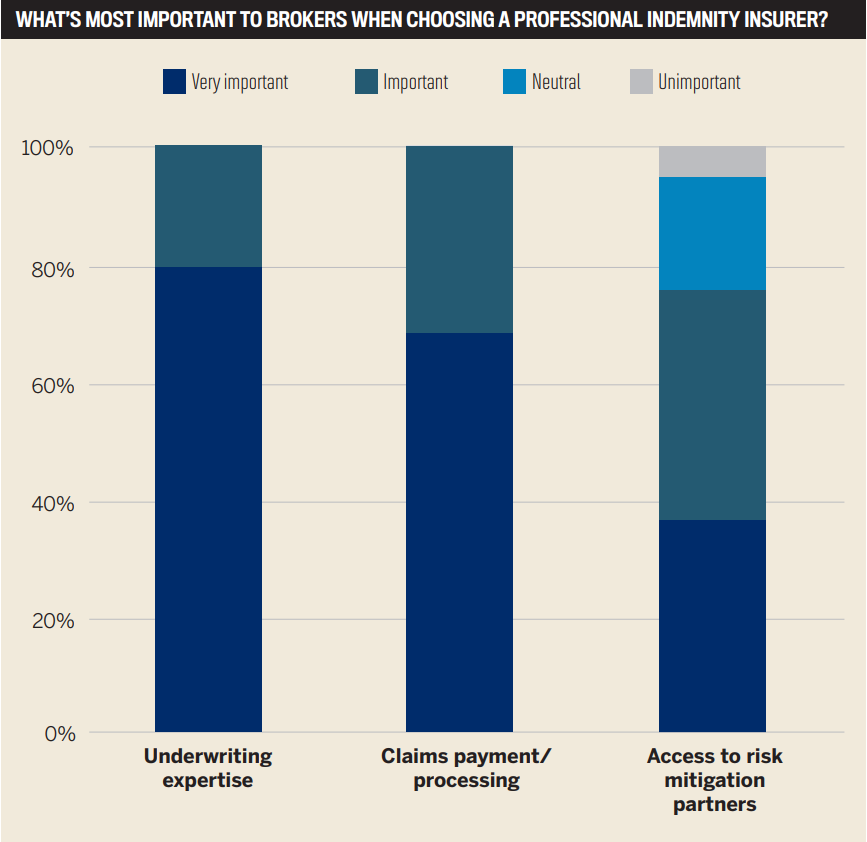

Picture source: Insurance Business Magazine “5-Star Awards 2021 : Professional Indemnity Insurers

Article Source: Insurance Business Magazine Australia ‘5-Star Awards 2021 : Professional Indemnity Insurers’

roulette222ee.com